![TS [UPDATED F.IMG] SEIS Tax Relief What Every Startup Investor Needs to Know - 072222](https://www.trendscoutuk.com/wp-content/uploads/2021/03/TS-UPDATED-F.IMG-SEIS-Tax-Relief-What-Every-Startup-Investor-Needs-to-Know-072222.png)

One reason why people invest in startups is that it qualifies them for the SEIS tax relief programme.

And whilst there are several online resources about SEIS. They primarily focus on explaining the tax benefits that startup investors can qualify for this programme.

In this article, I will explain to you everything you need to know about SEIS tax relief such as its benefits, risks and rules.

What Does SEIS Stand For?

Introduced by HM Revenue & Customs (HMRC) in April 2012, the SEIS (Seed Enterprise Investment Scheme) was developed by the United Kingdom government to help small, early-stage companies raise funds by providing a number of tax reliefs on investments made into qualifying companies through individual investors.

SEIS provides some of the world’s best tax reliefs. This allows up to 50% of your investment to be claimed back in income tax relief. And also offers significant capital gains tax reductions.

For startups, SEIS helps you raise the money you need to grow when your startup is at an early stage by offering significant tax reliefs to investors in your company, making a potential investment into your business more attractive.

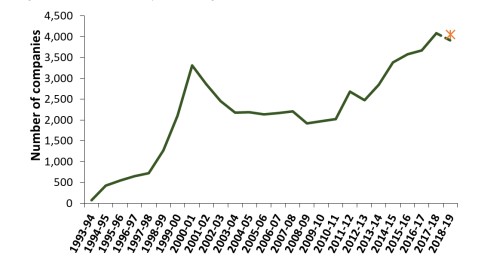

In 2018-19, a total of 1,985 companies received investment through the Seed Enterprise Investment Scheme (SEIS), and £163 million in total worth of funds were raised.

Over 1,500 of these companies were raising funds under SEIS for the first time, raising a total of £140 million in investment.

Also, the average investment per company under SEIS in 2018-19 was around £82,000.

Figure 1. A number of companies raising funds under SEIS from 2012-13 to 2018-19.

SEIS vs EIS

SEIS and EIS have always served the same essential purpose: to be a channel for early-stage investments to turn in high growth potentials.

However, although SEIS and EIS are very similar in many aspects, there are some differences you need to know.

The key difference is that the requirements for startups wishing to be part of either SEIS and EIS are different.

SEIS is explicitly targeted at startups and very early-stage companies. At the same time, EIS can be used by larger and older companies (although these are still considered as small and young in the context of the business and corporate landscapes in the UK).

SEIS is very much focused on very early-stage companies. And also allows an individual to invest up to £100,000 per tax year and receive a 50% tax break in return.

If you invest in SEIS, you will also profit from a capital gains tax exemption on any revenues that arise from the sale of the shares after three years.

Similarities of SEIS and EIS includes having no inheritance tax to pay on shares held for at least two years. Also, if your shares are sold at a loss, you may offset the loss against their capital gains tax.

How Does SEIS Work?

SEIS is intended to help your company raise capital as it begins to trade by providing tax reliefs to individual investors who obtain new shares in your company with tax relief.

A maximum of £150,000 can be acquired through SEIS investments.

This includes:

- any other de minimis state aid received in three years up to and including the date of the investment

- count towards any limits for later investments through other venture capital schemes: The Enterprise Investment Scheme (EIS), Social Investment Tax Relief (SITR), and Venture capital trust (VCT).

There are also various rules you must follow so your investors can claim and keep SEIS tax reliefs relating to their shares.

For instance, if you do not obey the rules for at least three years after the investment is made, tax relief may be withheld or withdrawn from your investors.

SEIS Tax Relief Examples

An example of SEIS Tax Relief is in these three scenarios:

Assuming an Income Tax rate of 45% and you owe Capital Gains at 28%, you invest £5, 000 and receive £2, 500 in Income Tax Relief.

If the company you invested in fails, your shares are worth £0, but you receive £1, 125 loss relief (50% investment x your tax rate).

When the company breaks even, you sell your shares for £5,000 after three years, having already claimed £2, 500 in Income Tax relief. You get £7, 500 back.

If the company doubles in value, your shares are worth £10,000. You won’t pay Capital Gains Tax on the profits from shares you’ve held for more than three years.

What are the Benefits Startup Investors Get from SEIS?

Income Tax Relief

‘Tax relief’ means you either:

- payless tax to take into consideration the money you’ve spent on specific things, like the expenses of your business if you’re independent/ self-employed

- get tax back or get it reimbursed in another way, like into a personal pension

You can get some types of tax relief automatically, but on some, you have to apply.

Pension contributions, charity grants, repair expenses, and time spent working on a ship outside the UK also applies to tax relief.

It also refers to work or business expenses. You may be able to:

- If you’re self-employed (a sole trader, limited company or partnership), you get tax relief on what you spend running your company.

- You use your own money in travelling and purchasing things that you need for your work.

Capital Gains Tax Relief

Capital Gains Tax is the tax on the profit when you sell or dispose of something (an ‘asset’) that’s increased in value.

In Capital Gains Tax Relief, it’s the gain you make that’s taxed, not the amount of money you receive

For example, you bought artwork for £10,000, and you sold it later for £50,000. This means you made a gain of £40,000 (£50,000 minus £10,000).

However, take note that some assets are tax-free.

You don’t need to pay on Capital Gains Tax on certain assets, including any gains you make from:

- Individual Savings Accounts (ISA) or Personal Equity Plans (PEPs)

- UK government gilts and Premium Bonds

- Gambling pools such as betting, lottery or pools winnings

The fact that investors don’t have to pay any capital gains tax on any income earned from investing in a SEIS company is one of SEIS’s main advantages. If you invest in a SEIS eligible business, then you will not need to pay capital gains tax on the income you make from that investment.

Capital Gains Tax Reinvestment Relief

A Capital Gains Tax Reinvestment Relief is a gain arising in the tax year 2019 to 2020 on disposal of any asset that is reinvested in shares in a company on which you get SEIS Income Tax relief.

Reinvestment relief permits an individual who has disposed of an asset. It would give rise to a chargeable gain – to treat a maximum of 50% of the gain as exempt from Capital Gains Tax. Where they have reinvested all or a part of the amount of the gain in qualifying SEIS shares.

You can also claim reinvestment relief if you get SEIS Income Tax relief on an acquisition of shares.

However, remember that you need to get SEIS Income Tax Relief before getting a reinvestment relief.

To obtain full reinvestment relief, you must invest in qualifying SEIS shares an amount at least equal to the chargeable gain. You can visit the Capital Gains Tax summary notes for more information on this. If you invest a lesser amount, reinvestment relief is limited to half the amount invested.

SEIS Loss Relief

An investment in SEIS offers loss relief. This enables you to offset losses obtained against either their Income Tax or Capital Gains Tax “CGT” amount.

At any point in time, if you make a loss on a disposal of your SEIS shares, you can set this loss against your chargeable gains.

To compute the loss, reduce the cost of your shares by the amount of any income tax relief given and not withdrawn.

You can claim loss relief on the year of the loss, then offset the loss against your current tax bill or the one for the previous year. You can offset your relief against either income tax or CGT.

Also, if the loss happens within the three year holding period and the company is wound up for genuine commercial reasons, the tax relief should not be withdrawn.

Deferral Relief

A deferral relief is the capital gains made on the disposal of an asset deferred by reinvestment in the Enterprise Investment Scheme (EIS), but not in the Seed Enterprise Investment Scheme (SEIS).

Investment in the EIS must be made in newly issued ordinary shares subscribed in cash.

Capital gains may be deferred if they have been made at the disposal of an asset not more than three years before or more than one year after the EIS investment is made.

Deferral relief does not depend on Income Tax Relief. More than £1 million can be invested in the EIS Income Tax Relief and get a deferral relief on the total investment.

It is also available where you do not satisfy the strict requirements of being unconnected with the EIS company. You can, for instance, be the company’s sole shareholder.

Under the following circumstances, will any deferred gains become taxable:

- An EIS company ends to qualify for any reason in the three years following the issue of the shares. In the three years from the commencement of trade, whichever is later.

- The EIS shares (unless sold to a spouse) are sold or disposed of.

- The EIS shares come to an end to be eligible shares within the three years of issue or three years of commencement of trade. Whichever is the latter?

- You become a non-UK resident within three years of the issue of shares or three years of commencement of trade (unless going to work full-time offshore for three years or less).

- You receive certain illegal benefits in the period starting one year before and ending three years after the issue of the shares or the start of trade, whichever is the latter.

- These illegal benefits can include directors’ remuneration, rents, loans or interest, which HMRC regards as excessive.

Inheritance Tax Relief

Inheritance tax is a tax on the estate (the property, possessions and money) of someone who passed away.

How much you pay is determined on the value of your estate – which is valued based on your assets (cash in the bank, investments, property or business, vehicles, payouts from life insurance policies) minus any debts and liabilities.

Usually, there is no tax to pay if either:

- Your estate’s value is below the £325,000 threshold.

- You leave everything over the £325,000 threshold to your spouse, civil partner, a charity or a community amateur sports club.

Your estate will, however, owe tax at 40% on anything above the £325,000 threshold when you die (or 36% if you leave at least 10% of the net value to a charity in your will) – excluding the ‘main residence’ allowance.

Furthermore, as long as you hold an investment in a SEIS-eligible business for more than two years before your death. Your SEIS investment would be exempt from Inheritance Tax.

Risks of Investing in SEIS Startups

Even when there are many advantages to investing in SEIS, there are also risks.

These risks include:

- The involvement of an individual in the company may be no more than 30%.

- Investors are locked in for a period of 3 years.

- As companies are not listed on the stock market, there’s no easy way to sell the shares.

SEIS Rules and Best Practices for Startup Investors

SEIS Investor Rules

When investing in SEIS, there are rules that you must follow:

Have UK income (but not requiring you to live there)

To claim SEIS, you don’t need to be a UK resident.

However, you must have UK income tax liability against which to set the relief.

The shares should be held for at least three years from the date of issue for the relief to be retained.

Relief may be withdrawn or reduced if within those three years they are disposed of, or if any of the qualifying conditions are not met before the shares’ termination date (3 years from the date of issue of the shares).

Not an employee of the company – but you can be a paid director

You and any of your ‘associates’ shouldn’t be an employee of the company up to the third anniversary from the date of the share issue.

An ‘associate’ consists of your business partners, trustees, and relatives (spouses, civil partners, parents, children, etc.)

However, your siblings are not considered associates.

Also, you can still be a director and receive a reasonable amount of compensation for this position.

No substantial interest in the company

You must not have any ‘substantial interest’ in the issuing company at any time from the incorporation of the company up to the third anniversary of the date of the share issue.

A SEIS’ Substantial interest’ is described as you directly or indirectly owning. Otherwise having an entitlement to obtain more than 30% stake in the company. Shareholdings of associates are also taken into account at the 30% figure.

No related investment arrangements

You would not qualify for a SEIS relief if you subscribed for the shares as part of a reciprocal arrangement that involves someone else subscribing for shares in a company in which you have a substantial interest.

No linked loans

At any point from the incorporation of the company until the third anniversary of the date of issue of the share. No loans should be made to you or your associates that are connected to your share subscription.

This includes instances where credit is given, or debt due from you or your associate is assigned.

No tax avoidance

You are not eligible for SEIS relief unless your subscription is for sincere business purposes. And also not as part of an arrangement or scheme which is the main reason or one of the main reasons is the avoidance of tax.

You can invest up to £150,000 under SEIS. However, there is a limit on the tax relief that you may use, which is capped at £50,000. Any amounts you invested exceeding £100,000 are not taken into consideration for the calculation of the income tax relief.

Withdrawal or reduction of the relief

Tax relief under SEIS may either be withdrawn or reduced if:

- Throughout the three years from the date of issue of the shares. You dispose of any of the shares (disposal to your spouse or civil partner is not counted);

- At any time from the company’s incorporation to the third anniversary of the date of the share issue, you obtain ‘value’ from the company or from a person linked to that company.

- The conditions during which you received value from the company include circumstances where the company would repay, redeem or repurchase any of its share capital belonging to you; the company repays a debt owed to you, the company provides a benefit or facility for you, etc. You can refer to the clarifications made by HMRC if you are unsure about whether you have received ‘value’ from the company.

- There is a call option or put option over the shares any time before date of the issue of the shares.

Lastly, take note that apart from the above requirements. You will not be able to claim your SEIS tax relief if the company doesn’t meet the requirements. Otherwise fails to spend the money raised by the share issue as needed.

Best Practices for Startup Investors

When you are investing in startups, the most important thing is don’t get lost in the hype.

Although some startups have been a source of huge returns. Most of them don’t last long or suffer a long time before fading.

You need to understand what distinguishes these, and while you can never be certain, you can at least know a few practices for startup investors.

Make Sure You (and others) Really Understand the Company

If you’re going to invest in a startup, it’s best to go for one that’s been pre-vetted.

Luckily, most of the services that allow regular individuals to get in on startup investing do that vetting for you. The analysis changes with each platform so make sure you look into the nature of that process. And also find something you are comfortable with.

That doesn’t take you off the hook though. Just because a startup is vetted doesn’t mean you invest in it right away.

Always examine the company carefully and see whether you still feel confident about its potential for growth.

Diversify (Carefully)

Diversification is always a good way to diminish risk. However, in a sector as unpredictable as startups, a blind “spray-and-pray” method probably won’t serve you well.

Try to diversify within a carefully curated group that spans many industries.

That way, you’ll be able to both provide serious capital for these companies. And also dodge the worst effects of any sector-specific volatile.

Invest What You Can Afford

Again, it can’t be emphasised enough that investing in startups is a risky game.

This is why you should only invest on what you can afford to lose.

You can figure this out by looking between 1% to 5% of your net worth. And also evaluating what you could lose within this range, given your current financial status.

Who Can Claim SEIS Tax Relief?

Investors, including directors, can claim initial tax relief of 50% on investments up to £ 100,000 with the Seed Enterprise Investment Scheme (SEIS) and Capital Gains Tax (CGT) exemption on any gains on SEIS shares.

You can claim SEIS Tax Relief when:

- You are not an employee of the company (but you are can be a director)

- Your stake in the company is not more than 30%

- SEIS tax relief applies only to recently incorporated companies

- The company must have 25 or fewer employees and gross assets of up to £200,000

- For 2012-2013 only, a Capital Gains Tax exemption will be offered in respect of gains realised on the disposal of assets that are invested through SEIS in the same year.

How Do You Qualify for SEIS Tax Relief?

To qualify for SEIS tax relief, your shares must be new. Ordinary shares are not redeemable and are not subject to special privileges.

Shares must also be paid in full and cash to qualify for Income Tax relief. You could not use a loan to buy the shares unless it was approved for the purchase of the shares.

How to Claim SEIS Tax Relief?

SEIS Claim Requirements

Before claiming a SEIS Tax Relief, you must have received a SEIS3 form from the company that you have invested in. This form serves as a confirmation of the amount you invested. And also states that the investment is qualified for tax relief.

If it has been trading for four months or if it has invested 70% of its overall investment. A company is issued SEISes by the SCEC (the Small Companies Enterprise Centre – a part of the HMRC).

The company then passes a SEIS3 form on to each investor. Who completes and submits it as part of their tax return.

When to File Your Claim

Tax relief can be claimed up to five years after January 31 for the year in which the SEIS investment was made.

Where to Send Your SEIS Claim Form

Once you receive your SEIS3 certificate, you will need to claim it in one of two ways:

- You do not need to give the SEIS certificate to HMRC along with your return if you are submitting your tax filings-you would only need to give it if they request it.

- If you aren’t submitting your tax filing, you need to complete pages 3&4 and send them to the office that manages your PAYE. You will find this information in any prior correspondence. You may have got it from HMRC, or this information should also be kept by your employer.

If you still don’t know where to send your SEIS certificate to, you can contact HMRC directly. They will be able to provide the right information for you.

Always keep in mind that HMRC may ask for your SEIS3 form even after you processed your taxes so be sure to keep it safe.

Where to Find SEIS Startups to Invest In?

Trendscout UK specialises in the government initiatives of Seed Enterprise Investment Scheme (SEIS).

Located in the heart of London, Trendscout is a platform that connects angel investors and founders, specialising in creating purposeful. Considered partnerships that drive profit and growth.

Every year, our team of experts study hundreds of startups. We analyse the potential, mission and ethical practices of every business we work with. Meaning every startup we represent will always align with our values.

Our network of innovative startups and investors. Combined with over 30 years of industry experience, allows us to identify up-and-coming opportunities before they reach the masses.

If you are interested in investing in SEIS, you can schedule an appointment with us today.

Rest assured that someone will get in touch with you and help you every step of the way.