![TS [UPDATED F.IMG] Enterprise_ _Investment_ _Scheme_ _(EIS)_ _ Explained_ _What_ _It_ _Is_ _And_ _How_ _It_ _Works_](https://www.trendscoutuk.com/wp-content/uploads/2022/08/TS-UPDATED-F.IMG-Enterprise_-_Investment_-_Scheme_-_EIS_-_-Explained_-_What_-_It_-_Is_-_And_-_How_-_It_-_Works_-071822.png)

Investing in small or emerging startups is complex since they require a long time to make a profit or repay your investment. Fortunately, the UK government’s Enterprise Investment Scheme (EIS) program provides attractive benefits to offset the risks of supporting fledgling businesses and opens up many opportunities for growing startups to raise additional funds.

Introduced by the UK government to boost its economy, these programmes are open to HNWIs and sophisticated self-certified investors to help them invest in startups with brilliant business ideas.

What is Enterprise Investment Scheme (EIS)?

The Enterprise Investment Scheme (EIS) is a tax-efficient investment to incentivise investment into smaller UK companies.

EIS was created to help smaller but high-growth-potential companies in raising funds by providing tax benefits to investors who invest in their company by buying their shares. Smaller companies benefit from this because they can raise funds to fund their growth, and investors benefit because they can invest up to £1,000,000 per year in qualified companies.

EIS allows you to raise £5 million yearly and a total of £12 million throughout your company’s lifetime. This also includes amounts received from other venture capital schemes. And within seven years following its first commercial sale, your company must receive investment under a venture capital scheme.

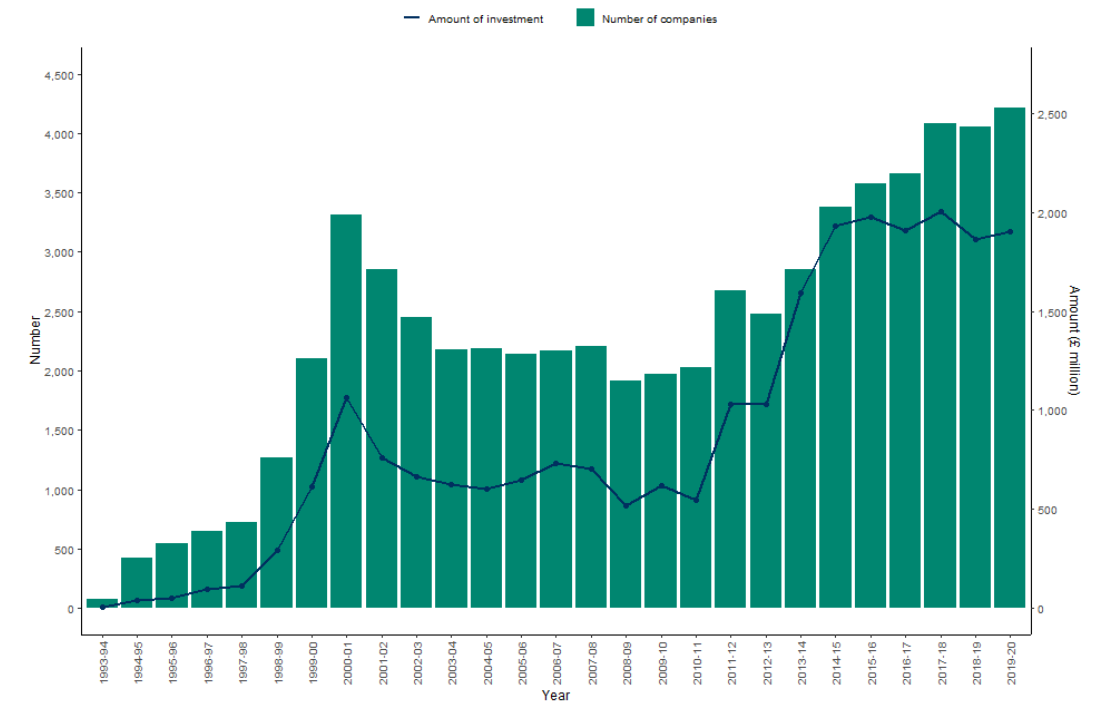

Since its launch, 32,965 companies have received funding, raising around £24 billion.

And in 2019 and 2020, 4,215 companies raised £1,905 million of funds through the EIS scheme. Funding increased from 2018 to 2019 when 4,060 companies raised £1,867 million.

Figure 1: Number of companies raising funds and the amount raised from April 1993 to 2020

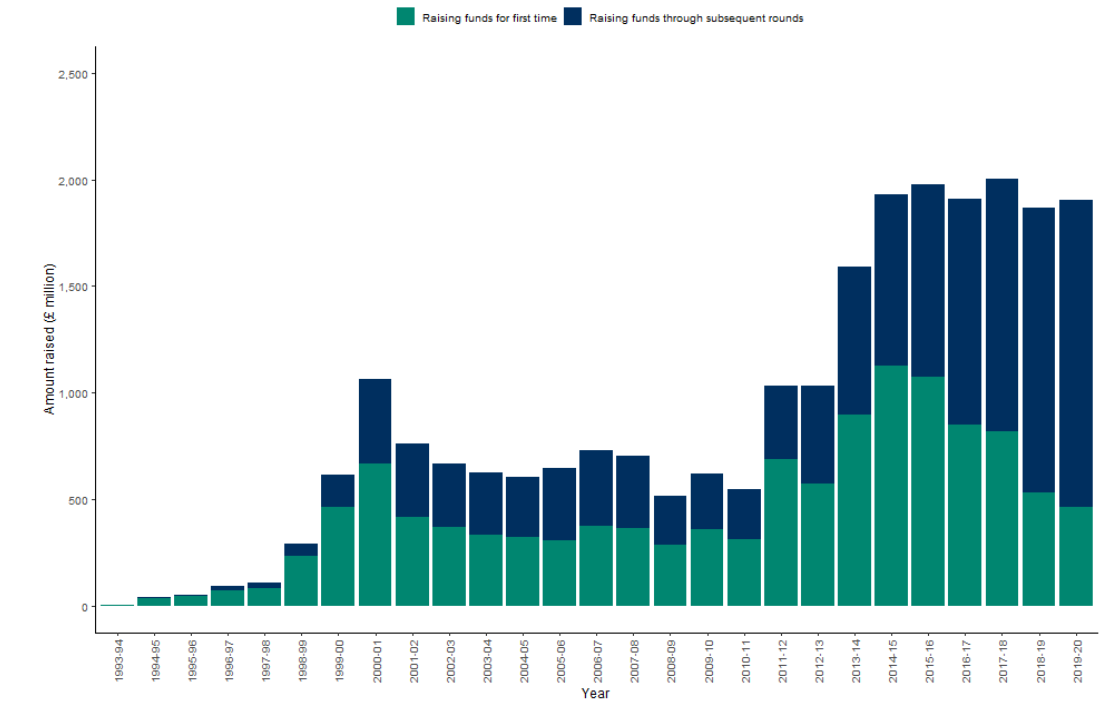

And from 2019 to 2020, a total of £466 million of investment was raised by 1,500 companies raising funds under EIS for the first time.

Figure 2: Amount of funds raised under EIS by new and old companies from April 1993 to 2020

Making an EIS-qualifying investment may improve your wealth while supporting the UK’s economic growth.

EIS vs SEIS

As part of the UK government’s ongoing initiative to encourage SMEs, the Enterprise Investment Scheme (EIS) and Seed Enterprise Investment Scheme (SEIS ) make UK-based enterprises more attractive investments. Recognising the difficulties that early-stage companies experience in raising the funding they need to grow, these programs offer generous tax breaks to investors ready to put their faith and money into these profitable businesses.

Here is a summary of the differences between EIS and SEIS:

| EIS | SEIS |

| It may be employed by more extensive and older businesses (although it is still considered small and young in the UK industry and corporate landscapes. | Aimed towards early-stage startups and businesses |

| Works well for sophisticated and more significant scale investors | Created to assist early-stage enterprises that would usually be too risky for all but the most adventurous investors |

| Trade must be at least seven years for the first round of funding | Trade must be at least two years for the first round of funding |

| Before investment, you may have up to £15 million in gross assets | Before investment, you may have up to £20,000 or less in gross assets |

| May have up to 250 employees | May have up to only 25 employees |

How Enterprise Investment Scheme (EIS) Works

You can invest in EIS in one of two ways: directly in a single EIS-qualifying company or through a fund manager who will develop a portfolio for you. Both options may have a place in the portfolio of a seasoned investor.

Investing in a single company gives you more visibility and control. Still, it also means more significant risks because your investment’s success depends on the fate of one company.

Meanwhile, investing in an EIS fund allows you to diversify your portfolio, usually within a specific area or sector. It also assures that a professional manager is researching and making investment decisions on your behalf.

You have less control and insight over where your money is invested with an EIS fund. Furthermore, because the fund manager’s knowledge is paid for, investment in a managed portfolio is typically more expensive than investing in a single company.

However, consider that all Enterprise Investment Scheme (EIS) investments are high-risk and should only be undertaken by experienced investors.

Before investing, ensure you thoroughly understand and examine the company. Always sift through the company to determine if you’re confident in its potential for growth.

Always remember the importance of developing a well-thought-out, meticulously constructed investing strategy. Before investing, ensure you understand and examine the company you want to invest in.

Enterprise Investment Scheme (EIS) Tax Relief Available

Below are some of the benefits startup investors and qualifying companies can get from EIS:

Enterprise Investment Scheme (EIS) Income Tax Relief

One of EIS’s leading tax benefits is Income Tax Relief.

Investors can claim 30% of their initial investment with income tax relief. The relief works by decreasing the investor’s income tax bill, knocking off an amount equivalent to 30% of the EIS-eligible investment.

Investors can claim up to £1 million in investments in a single tax year, equating to £300,000 of income tax relief.

Investors are also eligible for tax relief in the tax year that money is invested into a company. This may differ from the year the investment is made due to its time to invest in an EIS fund.

Capital Gains Tax (CGT)

The capital gains tax (CGT) is a tax on profits you make from selling assets. All financial gains above £6,000 are subject to CGT (your vehicle or your primary residence as an exception). Your tax band determines your pay, ranging from 10% to 28%. Most investors would have to spend at least 20% CGT on their gains.

Enterprise Investment Scheme (EIS) Tax-free growth

If you have claimed income tax relief on Enterprise Investment Scheme (EIS) shares and the companies still qualify, you usually don’t have to pay CGT.

When investors sell their EIS shares, any growth in value from an investment is tax-free.

To qualify, income tax relief must have already been claimed and not withdrawn by HMRC. Additionally, investors must keep the shares for a minimum of three years, and the company must remain EIS-qualifying for at least three years.

Capital Gains Tax deferral relief

CGT deferral aims to encourage additional Enterprise Investment Scheme (EIS) investment.

EIS gives a second relief affecting Capital Gains Tax. This relief allows investors to defer paying CGT on any asset if the gain from the disposal of that asset is used to purchase shares in another EIS-eligible firm.

Gains from the sale of EIS shares must have been made within a year of the EIS investment or within three years to qualify for CGT deferral. And only the amount invested in the EIS company allows for the tax break.

The gain will be deferred until the earliest of one of the following:

- EIS shares have been sold.

- Within three years of investment, the company ceases to be EIS-qualifying.

- Within three years of investing, an investor ceases to be a UK resident.

Enterprise Investment Scheme (EIS) Loss relief

EIS Loss Relief reduces the impact of losses on Enterprise Investment Scheme (EIS) investments. Net of tax relief, investors can offset up to 45% of this loss.

With two options, investors can cover any losses, which can be offset by their income or capital gains tax bill.

How the money raised through EIS can be used

The funds raised by the new share issue must be used for one of the following qualifying business activities:

- a qualifying trade

- getting ready to carry out a qualifying trade (which must start within two years of the investment)

- research and development that will result in a qualifying trade

The money raised by the new share issue should:

- Not be used to purchase all or a portion of another company

- Cause the investor’s capital to be at risk

- Be used to expand or develop your company

- Be spent within two years of the investment or within two years of the date you began trading

Criteria to be eligible for EIS

Both companies and their investors must follow specific regulations to qualify for EIS tax relief. The extensive EIS requirements are designed to keep businesses and investors from misusing the law and undermining its goal of encouraging small business investments.

For the company

Here are the requirements a company must fulfil to be deemed EIS eligible:

- The company has a permanent establishment in the UK.

- The company does not intend to be listed on a recognised stock exchange when issuing shares.

- Except for certified subsidiaries, the company has no authority over another company.

- No other company may possess or control more than 50% of the shares in the qualifying company.

- Before any shares are issued, the qualifying company and any of its subsidiaries must have no gross assets worth more than £15 million and no more than £16 million.

- The company must have fewer than 250 full-time employees when the shares are issued.

Knowledge Intensive Companies (KICs)

Knowledge Intensive Companies (KICs) are treated differently.

Described as companies whose primary business activity is research and development (R&D), knowledge-intensive corporations (KIC) are now eligible for more EIS financing than other businesses, thanks to the Treasury’s Autumn Budget 2017.

For investors

Here are the criteria you must meet to be eligible for EIS as an investor:

- Your interest in the company must be less than 30%.

- You must not be a paid director, partner, or employee of the company.

- Your business partners or associates (spouse, relatives, or previous business contacts) are not interested in the company.

- You don’t have any preferential shares, and you don’t have any controlling interest in the company.

- You aren’t using the plan to avoid paying taxes.

One exemption to the rule is prohibiting related persons from working in the business. This exemption encourages business angels to participate in the scheme because of their roles as directors. Even if paid, business angels may be eligible for a tax reduction if the angel director was not affiliated with the company when the shares were released. Because business angels’ requirements are strict, obtaining assistance from HMRC is preferable.

Summary

EIS is a scheme created by the UK Government to help startups and businesses find investors willing to risk their funds for success. It provides a safety net for investors, making them more willing to take a chance to profit from innovation.

Still, investors should carefully consider and understand the benefits and risks of investing in EIS.

If you’re interested in investing in EIS, you can schedule an appointment with us today.

We specialise in the government initiatives of the EIS.

Based in the heart of London, we connect angel investors and founders, building purposeful collaborations that generate profit and growth.

We have over 30 years of industry experience and a network of creative entrepreneurs and investors, allowing us to spot up-and-coming prospects before they hit the masses.