Investing in small or new businesses is a risky venture.

Companies not listed on a stock exchange hold an exceptionally high risk of losing capital and small companies also take a long time to recoup investment or generate profit.

Fortunately, EIS provides investors attractive benefits to counterbalance the risks of supporting fledgeling businesses.

EIS provides various advantages, such as incentivising investors to invest in early-stage companies by offering them significant tax advantages.

A 30% tax relief can be received on their investment, and they are exempt from paying capital gains tax on any profits they made after selling their shares after three years.

What is EIS?

The Enterprise Investment Scheme or EIS is a UK government scheme that encourages investors to fund early-stage, higher-risk businesses by providing generous tax reliefs.

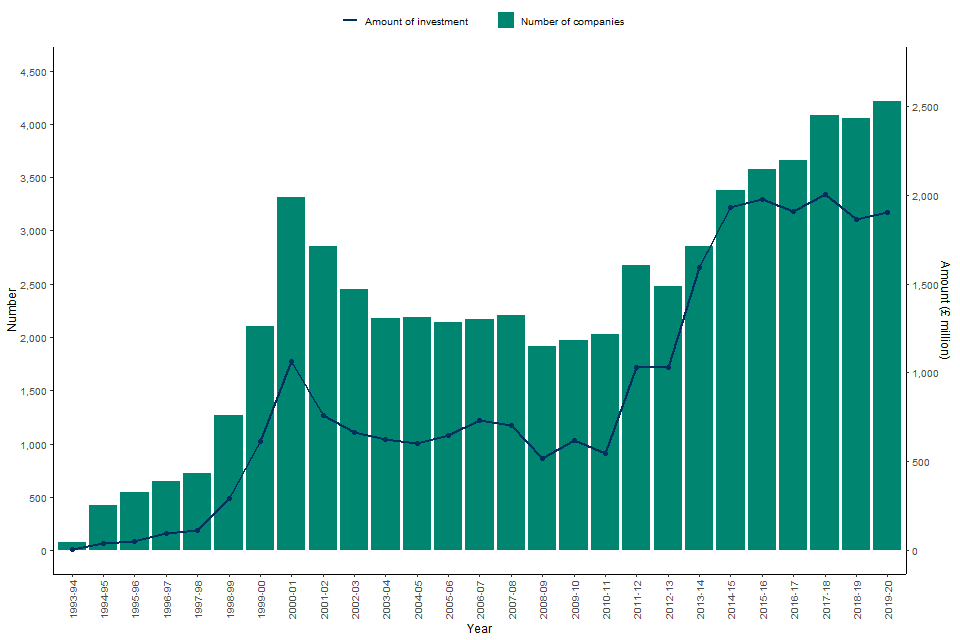

EIS was launched in 1994 by the UK government and is a well-established part of the UK tax landscape for investors.

Since then, 32,965 companies have received investment, and around £24 billion of funds have been raised.

Figure 1: Number of companies raising funds and amount raised, April 1993 to 2020

How Does EIS Work?

You can invest in EIS in one of two ways: investing directly in a single EIS-qualifying company or through a fund manager who will develop a portfolio for you. Both options may have a place in the portfolio of a seasoned investor.

Several tax incentives are also available to investors and qualifying companies under the Enterprise Investment Scheme.

Income Tax Relief

Income Tax Relief is one of the leading tax benefits provided by EIS.

Investors can claim 30% of their initial investment with income tax relief. The relief decreases the investor’s income tax bill knocking off an amount equivalent to 30% of the EIS eligible investment.

Capital Gains Tax

Capital Gains Tax (CGT) is the tax on your profits from selling any assets.

CGT applies to all financial gains above £6,000 (with your vehicle or your primary residence as an exception). Your tax band determines the amount you pay, varying from 10% to 28%. Most investors would have to spend at least 20% CGT on their gains.

Capital Gains Tax Deferral

EIS provides a second relief affecting Capital Gains Tax. This relief allows investors to delay paying CGT on any asset if the gain from the disposal of that asset is used to buy shares in another EIS-qualifying company. CGT deferral aims to promote additional EIS investment.

To qualify for CGT deferral, gains from the selling of EIS shares must have been made within a year before or within three years after the EIS investment. The relief is restricted to the amount invested in the EIS company.

Loss Relief

Investing in early-stage startups entails a high level of risk.

Fortunately, EIS Loss Relief minimises the impact of losses on investing in EIS companies.

Investors can cover losses on an EIS company by claiming loss relief with two options. The loss can be offset by the investor’s income tax bill or capital gains tax bill.

Inheritance Tax Relief

Inheritance tax is a tax on a deceased person’s estate (their land, assets, and possessions).

Suppose the value of your estate is below the £325,000 threshold, or you leave anything above the £325,000 threshold to your spouse, civil partner, a charity, or a voluntary amateur sports club. In that case, there is usually no inheritance tax to pay.

You can claim inheritance tax relief of up to 100% after owning EIS shares for two years. This benefit is applicable only if the shares are not listed on a recognised stock exchange.

Tax-Free Growth

If you have claimed income tax relief on EIS shares and the companies still qualify, you usually don’t have to pay CGT.

When investors sell their EIS shares, any growth in value from an investment is tax-free.

To be eligible, income tax relief must have already been claimed and not withdrawn by HMRC.

Additionally, you must keep the shares for three years, and the company must remain EIS-qualifying for at least three years.

Carryback

A “carryback” facility allows all or part of the cost of shares purchased in one tax year to be counted as if they were purchased in the previous tax year. The relief is then applied to the last year’s income tax liability rather than the tax year in which the shares were acquired. This is subject to the overriding limit for relief for each year.

EIS Tax Relief Examples

An example of EIS Tax Relief is in these three scenarios:

When your investment performs well and triples in value over the course of 3 years

- Your initial investment = £20,000

- Income tax relief (30% of your investment) = £6,000

- Your investment returns (after 3 years) = £60,000

- Capital gains tax (on the sale of shares) = £0

Suppose you invested £20,000 in an EIS-eligible company.

You can claim income tax relief on 30% of the amount of your investment, saving you £6,000.

After three years, you profit from your investment and do not pay capital gains tax if you sell your shares.

Your investment returns after three years would be £60,000 with a total return of £66,000.

When your investment stays the same value over the course of 3 years

- Your initial investment = £20,000

- Income tax relief (30% of your investment) = £6,000

- Your investment returns (after 3 years) = £20,000

- Capital gains tax (on the sale of shares) = £0

Although your investment didn’t rise in value, the income tax relief resulted in a £6,000 gain.

When your investment performs poorly, and the value of your shares goes to zero

- Your initial investment = £20,000

- Income tax relief (30% of your investment) = £6,000

- At risk capital = £14,000

- Loss relief (with income tax at 45%) = £6,300

- Total returns = £12,300

Rather than losing the total amount of your £20,000 investment, EIS tax relief means your loss is reduced to £7,700 due to both the income tax relief on your initial investment (£6,000) and the loss relief (£6,300).

What are the Benefits Startup Investors Get from EIS?

EIS incentivises investors to invest in early-stage companies by offering significant tax advantages.

If you’re an EIS investor, you can receive a 30% tax relief on your investment and are exempt from paying capital gains tax on any profits after selling your shares after three years.

Also, you’re not subject to inheritance taxes for shares owned for at least two years. You also could deduct the loss from their capital gains tax if the shares are sold at a loss.

Meanwhile, EIS benefits you as a business by making your company a more attractive and less risky investment opportunity.

How Much Can Investors Invest Under EIS?

The amount that every individual investor can invest is limited due to the significant tax relief granted to investors under EIS and SEIS.

With EIS, each investor can invest up to £100,000 per tax year. You can also raise up to £5 million each year and a maximum of £12 million in your company’s lifetime. Amounts obtained from other venture capital schemes are also included.

Risks of Investing in EIS Startups

There are always risks involved in any financial gamble.

With EIS, it is the same as supporting any small business – they are more likely to fail than a larger corporation. Tax relief is also dependent on an individual’s circumstances. It’s subject to adjustment in the future, and the availability of tax relief is contingent on the amount invested in maintaining its qualifying status.

However, always remember that the upside is that if you invest in a business early on and succeed, you can have a higher return.

EIS Rules and Best Practices for Startup Investors

EIS Investor Rules

It’s a complex scheme. Along with the standard stipulations, each EIS tax relief branch has its own criteria.

The following investor rules apply to any claim for EIS:

- You can spend only a maximum of £1 million on qualified companies per tax year (the number of qualifying companies is not limited)

- Your shares must be held for at least three years

- You may not carry forward your EIS tax relief

- You’re a UK taxpayer

- You’re not affiliated to the EIS company either as an employee, partner, or remunerated director.

Best Practices for Startup Investors

Invest What You Can Afford

It can’t be emphasised enough that investing in startups entails high risks.

This is why you should invest only in what you can afford to lose.

Considering your current financial situation, look between 1% to 5% of your net worth and evaluate how much you could lose within this range.

Ensure You Understand and Examine the Company

Always sift through the company to see if you’re confident in its growth potential.

Conceptualise a thoughtfully designed, carefully constructed investment plan. Make sure you understand and examine the business before investing.

A Well-Research Market

Research and understand the industry you wish to join and its key players and potential competitors.

Knowing how much the demand for a product is crucial to a startup’s success. It is essential to conduct extensive research of the target market base before an accurate picture of demand forms.

Who Can Claim EIS Tax Relief?

You could claim EIS Tax Relief if you obtained an EIS certificate indicating that HMRC has approved your investment in a qualifying company.

Although there could be a delay in securing the certificate since a company must have been trading for at least four months, at least 70% of the funds raised have been spent.

How Do You Qualify for EIS Tax Relief?

Whether you’re a business trying to attract an investor through the EIS scheme or an investor hoping to profit from tax benefits, check if you meet the criteria before applying.

To qualify for EIS tax benefits, the corporation and the investor must meet specific additional requirements.

Investor

To be eligible for EIS as an investor, you must meet the following criteria:

- Your interest in the company must be less than 30%.

- You must not be a business employee, partner, or paid company director.

- Your partners or associates do not have any interests in the company (this includes your spouse, relatives or previous business contacts)

- You don’t have any preferential shares of any kind.

- You don’t have any form of controlling interest in the company.

- You aren’t using the scheme for tax avoidance.

The rule disqualifying related persons working in the business has one exception.

Given their positions as directors of the corporation, this exemption helps to promote participation from business angels in the scheme. Even if compensated for their services, business angels could be liable for tax relief if the angel director was not related to the company when the shares were released.

However, since the rules for business angels are strict, it’s best to seek HMRC advice.

Company

To be eligible for EIS, the company in which an investor invests must fulfil the EIS eligibility criteria and retain that status for the shareholding duration.

The following requirements must be fulfilled for a company to be deemed EIS eligible:

- The company has a permanent establishment in the UK.

- The company is not listed on a recognised stock exchange or intends to be listed when issuing shares.

- The company has no control over other companies except for qualified subsidiaries.

- No other company may own the qualifying company or own 50% or more of its shares.

- The qualifying company, as well as any of its subsidiaries, has no gross assets worth more than £15 million before any shares are issued and not more than £16 million after

- The corporation must have fewer than 250 full-time employees when issuing shares.

In addition to these criteria, the investment must be put to good use in a qualifying trade.

Most business practices are permissible, but some of the trades are not. If these excluded trades account for more than 20% of its regular operations, it would be ineligible for the program.

The following activities are examples of those that are not permitted:

- Production of coal or steel

- Farming or market gardening

- Forestry

- Legal or financial services such as banking and insurance

- Leasing or property development

- Energy generation

- Exporting electricity

- Offering services to a non-qualifying company

If your company engages in any of the above-mentioned excluded trades, consider consulting HMRC about your eligibility for the scheme. This can be accomplished by requesting “advance assurance.” HMRC will assess the company’s day-to-day operations to see whether it meets the qualifying trade requirements and decide if you are entitled to file a claim.

However, if HMRC accepts that you are likely to qualify for EIS, this is an opinion, not a guarantee.

Knowledge Intensive Companies (KICs)

Knowledge Intensive Companies (KICs) are treated differently.

Described as companies whose primary business activity is Research and Development (R&D), knowledge-intensive corporations (KIC) are now eligible for more EIS financing than other businesses, thanks to the Treasury’s Autumn Budget 2017.

How to Claim EIS Tax Relief?

EIS Claim Requirements

Before you can claim tax relief, you must have obtained an EIS certificate indicating that HMRC has approved your investment in a qualifying company.

After receiving the S/EIS3 certificate, you can claim it in one of two ways:

- You don’t have to give the EIS certificate to HMRC with your tax return if you’re submitting your tax filings; you’ll have to send it if they ask for it.

- If you’re not submitting your tax filing, you must complete pages 3&4 and send them to the office that deals with PAYE. This information can be found in any prior correspondence you may have received from HMRC, or your employer should hold this information.

When it comes to claiming tax relief, there are a few things to keep in mind:

Share “Termination Date”

EIS shares must be owned for three years to qualify for income tax relief, so they should be considered long-term investments.

The share termination date on your EIS certificate is when you must retain your share. If you sell your shares before holding them for three years, you must notify HMRC and refund any income tax relief you have claimed.

Investor Tax Reference

Not all investors will have an investor tax reference number.

Instead, provide your National Insurance Number so that HMRC can link your claim for tax relief to your income tax.

Tax Relief for a Different Year

According to HMRC, there is a possibility to back-date the tax relief claim to earlier tax years.

A ‘carry back’ facility allows you to classify all or part of the expense of shares purchased in one tax year as though they were purchased in the previous tax year.

Relief is thus given against the prior year’s income tax liability rather than the tax year in which the shares were purchased. This is subject to the overriding limit for relief for each year.

When to File Your Claim

EIS Tax Relief claims can be made for up to five years after the first 31st of January following the tax year in which the investment was made.

Where to Send Your EIS Claim Form

If you invested in shares issued during the year for which you haven’t yet received a form EIS3 or EIS5, you wouldn’t be able to claim relief until you’ve received a form. If you receive the form after you’ve sent your tax return, complete the claim form inside the EIS3 or EIS5 and send it to HMRC.

Consult a Financial Adviser

Investors must consult a financial adviser to help them find an EIS investment that fits their investment goals and financial limitations.

Also, a financial adviser will assist you with the claim if necessary.

For example, the EIS 3 Certificate is needed before a claim for any of the EIS tax reliefs can be made. You can complete the claim form you receive (found on pages 3 and 4 of the EIS3) and send it to your HMRC tax office.

With this, a financial adviser may be able to assist you in claiming your tax relief or if you have any other questions.

Where to Find EIS Startups to Invest In?

Investors should carefully consider and understand EIS’s benefits and risks.

Trendscout specialises in the Enterprise Investment Scheme (EIS) government initiatives.

Based in the heart of London, we connect angel investors and founders, building purposeful collaborations that generate profit and growth.

We have over 30 years of industry experience and a network of creative entrepreneurs and investors, allowing us to spot up-and-coming prospects before they hit the masses.

Rest assured that our team will be with you at every step of your investment journey.

Originally published April 12, 2021, 08:08: AM, updated March 28, 2022